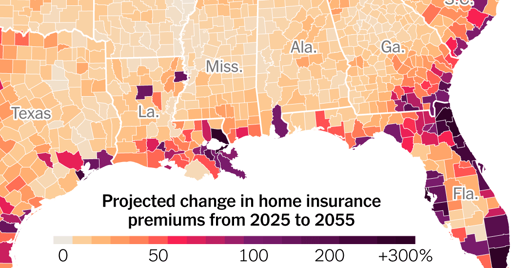

Average premiums have risen 31 percent across the country since 2019, and are steeper in high-risk climate zones. Over the next 30 years, if insurance prices are unhindered, they will, on average, leap another 29 percent,

More likely, over next 6 years will match increase since 2019. Taxpayer subsidies of insurance doesn’t count. Neither does Florida type “deregulation” which makes it easier for insurance to avoid paying claims.

Other quote from article is that insurance is now 20% of a mortgage payment. A 30 year amortization at 5.31% means total interest payments equal to loan. Current interest rates are about 2% higher than this. But historical home appreciation is 3%, and when mortgage rates are above 3%, then you fundamentally expect to lose money except for the distortions of taxes on interest payments vs rent. Rent avoidance + interest tax credits can still make ownership attractive, but at least balanced long term vs rent alternatives.

That 20% of mortgage payment though is equivalent to 1.33% on full home value. Up from 0.5%. OP is projecting it will rise in some parts of the country to over 5% of value. Which is about right for what used to be 500 year events happening less than every 10 years. Insurance could go up much quicker and to higher levels since global warming means even worse than current disaster levels.

But the expectation of historical 3% annual home appreciation, goes straight to 1.5% depreciation expectations when insurance goes from 0.5% to 5% of value. Construction cost inflation is also insurance (because of “value” and replacement cost) inflation. Home prices are currently overvalued due to high interest rates making people not being able to afford trading up in homes due to high mortgage costs, and so not selling their home, limiting supply. Very low new construction levels due to same effect. One effect of mass deportations is lower home values due to fewer tenants, while also keeping interest rates high due to less cheap labour availabe, inflation. Tariffs/war on Canada means vast Canadian 2nd homes in US up for sale.

Housing depreciation will cause banking collapses and recessions, leading to more housing depreciation. Bankster bailouts (banks are the important people) reduce US financial credibility even more, and even higher interest rates to depreciate home values more with more bank bailouts.

More likely, over next 6 years will match increase since 2019. Taxpayer subsidies of insurance doesn’t count. Neither does Florida type “deregulation” which makes it easier for insurance to avoid paying claims.

Other quote from article is that insurance is now 20% of a mortgage payment. A 30 year amortization at 5.31% means total interest payments equal to loan. Current interest rates are about 2% higher than this. But historical home appreciation is 3%, and when mortgage rates are above 3%, then you fundamentally expect to lose money except for the distortions of taxes on interest payments vs rent. Rent avoidance + interest tax credits can still make ownership attractive, but at least balanced long term vs rent alternatives.

That 20% of mortgage payment though is equivalent to 1.33% on full home value. Up from 0.5%. OP is projecting it will rise in some parts of the country to over 5% of value. Which is about right for what used to be 500 year events happening less than every 10 years. Insurance could go up much quicker and to higher levels since global warming means even worse than current disaster levels.

But the expectation of historical 3% annual home appreciation, goes straight to 1.5% depreciation expectations when insurance goes from 0.5% to 5% of value. Construction cost inflation is also insurance (because of “value” and replacement cost) inflation. Home prices are currently overvalued due to high interest rates making people not being able to afford trading up in homes due to high mortgage costs, and so not selling their home, limiting supply. Very low new construction levels due to same effect. One effect of mass deportations is lower home values due to fewer tenants, while also keeping interest rates high due to less cheap labour availabe, inflation. Tariffs/war on Canada means vast Canadian 2nd homes in US up for sale.

Housing depreciation will cause banking collapses and recessions, leading to more housing depreciation. Bankster bailouts (banks are the important people) reduce US financial credibility even more, and even higher interest rates to depreciate home values more with more bank bailouts.