How can a community dedicated to housing bubbles not understand what caused the 2008 crash? It had nothing to do with the # of houses up for sale. It was the coreupt flexible rate mortgages being issued for a decade before 2008 that caused it. Where do you get that from a fuckin chart that only shows the quantity of houses being sold?

You are talking about two different markets in this comment though:

- CLO/MBS securities, some of which contained variable rate mortgages

- buying/selling residences

1 crashed as results of 2 fail, ie people stop trading due to jobs issue.

Coming back to 2024, we are in only got 2 in play. People are not really buying or selling houses because people don’t get paid enough to justify the current price v monthly expense. Either price goes down or interest. It does not have to be economic doom unless something else fails along with it.

Sure, but there’s tons of homes now that are not cash flowing and are only being held on by investors because of the equity they have.

If inventory keeps rising and prices fall it could trigger a rush for the exits.

Lol where do you get that from houses being for sale? Or are you adding your own context? If that’s the case do you have anything you can provide a link that supports this? Not being contradictory, would like to see why there are so many investment properties hitting the market.

Because if there’s a ton of supply then sellers have to get more competitive. It’s already happening on the new build side. You can get every upgrade practically for free, big buy downs on interest rate, etc.

But how are you getting that from the graph is all I’m asking. That is a hardly even speculative without anything to indicate all these sellers aren’t in the market to buy another house in the same area. You would need some indication they were all leaving the area or selling to move into a rental.

volume

There’s a ton of exotic DSCR loans underwritten by private equity firms that have HIGH interest rates. They may not be as pervasive as ARMs were in '08 but there’s more than enough of them to effect the market if they collapse.

It’s a myth that people there’s tons of people who won’t give up their “4% mortgage”. Only well capitalized investors could get that. Most investors paid way over both on price and financing through doggy private equity financing. You don’t know what you’re talking about.

My b I didn’t see you responded back to original comment. If this is common knowledge in that area than I suppose but you still haven’t shown where you are drawing this information from and even admit the mortgages now are better than 2008. Not really sure why your getting pissy saying I don’t know what I am talking about when all I’m asking is where you are drawing your information from when all that was given is a chart showing volume of houses on the market. Either way hope your night gets better than whatever put you such an abrasive mood🍻

That’s untrue, sub 4 was completely available to qualified buyers of “normal” status/income.

For rentals? For borrowers with little to now down? Not really. And these borrowers didn’t stop with one rental, they’d get several sometimes dozens. That’s why you saw so many real estate Tik Tokers during the pandemic.

Where did rentals come up? I’m discussing purchases.

I don’t get information from TikTok, I get it from professionals

Exotic loams liken DSCRs are only used to buy investment properties. Investor demand is what’s driving the shortage and exploding home prices. Just like in '08.

Yes many primary residency borrowers got 4 percent on traditional loans. But investors didn’t because they were in a buying frenzy from 2019-2022. They couldn’t wait for traditional mortgages, these were the supposed “cash buyers” that were infamously waiving inspections and appraisals. The FHA isn’t going to let you do that.

Go ahead and get your news from “professionals” who were denying the existence of a bubble at all until this month.

I’m more of a silt guy

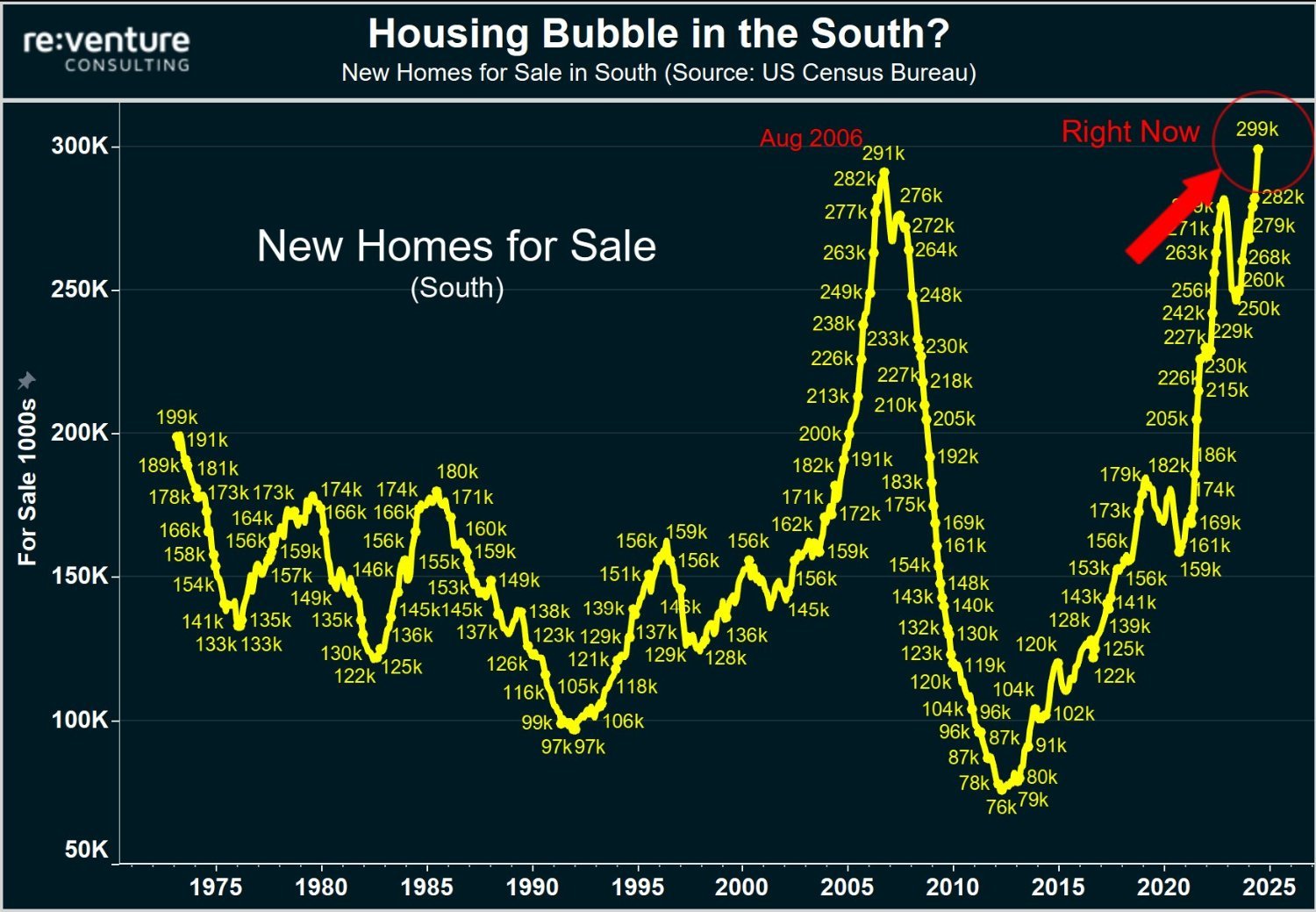

I’m decently close to real estate and everything I’m seeing is low low inventory. I’d love for this chart to be true I just haven’t seen it.

I am currently in Florida and all I see are empty homes and “for sale” signs. Two weeks ago I stayed in Longboat Key and half to two thirds of the homes in the neighborhood I was staying in were for sale.

Cuz fl is a shithole

And I’m in NW Florida and am only aware of a single home for sale in my hood.

That is the problem with stats that are zoomed out. It would be more helpful if you could visualize which counties and zip codes have the most inventory as well as the median “days on market”.

Could this be in an area that’s been deemed uninsurable? IIRC there’s whole areas where you just can’t insure your house any more.

Are you in the south US?

I actually don’t know. New Mexico so it’s kind of south? Haha

I also wasn’t sure what region I fell in but thankfully there’s a map.

I don’t think the Southwest is considered part of the South.

Wait what? You don’t know the basics about your home state?

Kind of? Lol education isn’t your states strong suit

Proofs?

I talk about similar things with my co-workers from time to time. Prices are high, but the risk isnt outside the range of normal, this isnt 2008 where there were tons of bad loans just a gnats hair away from defaulting.

If someone can explain how a bubble can exist right now or what would cause prices to go down, please let me know (or resources where I can read more on it).

I could see a bubble of too many homes for sale and not enough people buying. Not really a huge crash but it would cause prices to ease up. I’m currently looking to buy a new home and the longer I wait the more I’m seeing prices continue to drop.

Except that is pretty region specific. I would understand that being the case in climate evacuation areas where the insurance market has fled. But in most parts of the country I have been led to understand that there are few people trying to sell because they have locked in good interest rates.

“My anecdotal experience definitely trumps statistical analysis”

True, but the OP has no data either. Just a pretty picture that they say is based on data.

Looks reasonably accurate to a country wide picture.

Thanks for the link. Doesn’t look like it’s as high as 2008 but getting there. It’s tough to buy with such high interest rates right now so not surprising.

Ironically, the fed is getting closer to lowering interest rates, because inflation is finally getting close to the numbers that they want to see. If interest rates drop, then mortgages suddenly get more affordable, which makes the market heat up again.

Strictly anecdotal, but there are multiple land-only properties in my area that have been on he market for years because building is too expensive. The guy that bought a parcel of land right next to ours planned on starting to build three years ago, and then two years ago, and then last year, and each time he ends up not being able to afford to build, because construction contractors are so in-demand right now that their rates are sky-high. So he’s paying taxes and HOA fees on land that he can’t do anything with.

By this same logic, someone in 2004-2005 could look back to the crash in the 80s and see they’re at the same level as that peak and a crash is imminent. In fact it was a year or two away and new homes for sale were going to go up another 50% before the crash.

That’s not to say that things looks good. Some sort of correction is probably coming but it could be another year or two or more.

I’m having a hard time finding info that supports this. Texas currently has just over 100k homes for sale - thats total homes, so new builds (as this chart shows) would be significantly lower. This is high, but definitely not the highest ever and it was higher 3x since 2018. I didn’t check the other southern states. I’m not saying it’s wrong, just that i couldn’t find support for it. If you do, please share.

Here’s the website that shows new homes for sale. It does verify 300k in the south. i didn’t expect the South (299k) to be over half of the total US (480k). https://www.census.gov/construction/nrs/data/series.html

If supply of homes for sale is high, buyers will have more choices, and therefore prices may stay flat… Or fall.

But this is housing, unfortunately. Retirees will want to maximize their investment. Sellers may choose to pull off the market if they can’t get a price that will let them get into their next home…

I don’t think high supply of houses for sale means a bubble. Hopefully for those trying to buy their first it means price growth has stalled.

If you don’t live in the house or rent it… It get expensive quick esp if prices are not going up.

Investors always sell first when market turns while some people have to sell and buy during life tho

Idk, I live in NC and the amount of homes that are for sale and have been for sale for a few months (generally due to high prices) are very, very high. I wouldn’t be surprised if it does fold, as it isn’t just retirees selling.

{kind=link}